Youth Leap Account After Program Changes: Keep, Close or Move to a Youth Future Savings Plan?

This English companion post explains the same topic in a localized format for international readers. It focuses on what the program, market issue or company means, what to check first, and which practical details should not be missed.

The goal is not a literal translation. It is a clear guide that keeps the original Korean context while making the topic easier to understand for readers who follow Korean housing, finance, policy, health or market news in English.

Quick overview

| Item | Key point | Why it matters |

|---|---|---|

| Product | Youth Leap Account | Long-term savings |

| Decision | Keep or close | Depends on benefits |

| Alternative | Youth Future Savings | Compare before moving |

| Risk | Early cancellation | May reduce benefits |

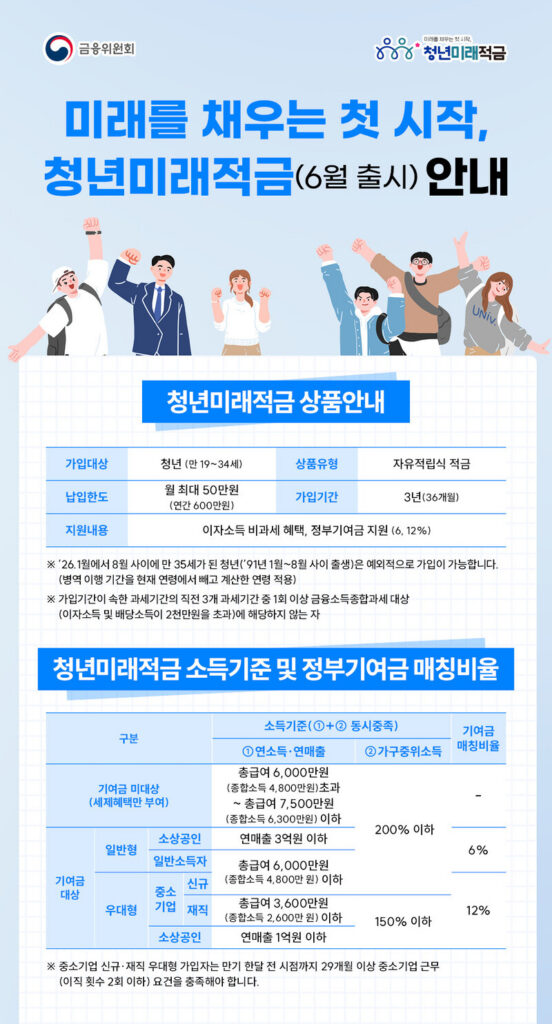

Why account holders need a decision plan

The Youth Leap Account was built as a long-term savings product for young adults, so decisions after program changes should not be made only from a headline. The key question is whether keeping the account preserves government contributions, tax benefits or favorable interest compared with closing it early.

When keeping the account may be better

Keeping the account may make sense if the remaining period is manageable, the benefit is still meaningful and early cancellation would reduce support. People who can continue monthly deposits without pressure should compare the maturity benefit with any new product before making changes.

When closing or switching may be considered

Closing or switching may be considered if household cash flow has changed, if monthly deposits are too burdensome or if a new product provides a better match. However, the loss of accumulated benefits can be larger than expected, so it is important to calculate the actual difference rather than moving automatically.

How to compare with Youth Future Savings

Compare monthly deposit limit, government contribution, interest rate, maturity period, income condition, age condition and cancellation rules. A product with a more attractive headline may not be better if your eligibility is uncertain or if the benefit period is shorter.

Bottom line: Read the official notice, account terms or company data before making a decision. The summary is useful for orientation, but eligibility, timing, tax treatment and investment risk must always be checked against the latest official information.

Frequently Asked Questions

Should I close my Youth Leap Account immediately?

Not necessarily. Compare remaining benefits, cancellation loss and alternative products first.

What should I compare?

Deposit limit, contribution, interest, maturity, eligibility and early-cancellation rules.

Is Youth Future Savings always better?

No. It depends on your eligibility and the benefits you would lose by closing the current account.

You can also browse more English policy and finance explainers on this site.